Housing affordability has become a federal political firestorm unlike at any other point in a generation. Credit: Marija Ercegovac

No matter how you do the math, the only way for housing to become affordable is for prices to fall or stop climbing.

But in a country where the single greatest source of household wealth is the family home and the land it sits upon, no one wants a 24-year-long party to end.

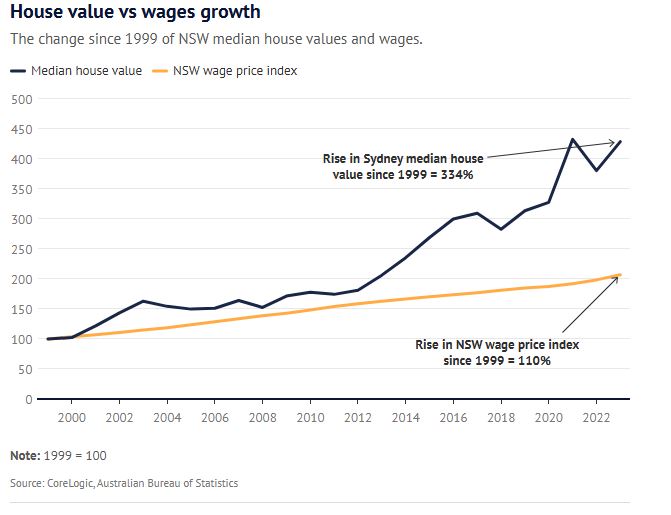

The graphs displayed here show the wicked problem. House and apartment values have easily outpaced wage growth since the turn of the century, forcing prospective home owners to take on increasingly large mortgages.

In a situation that independent economist Nicki Hutley describes as criminal, and fellow economist Saul Eslake warns will worsen, wages have grown by about 110 per cent since 2000 while inflation has increased by about 100 per cent.

But house values have climbed by between 330 and 411 per cent in our capitals over the same period. Despite the lift in wages over the past two years, the gap is widening as house values climb even faster.

The gap between wages and house values has been made up by super-sized mortgages.

By the end of 2000, the average new loan was $111,000. Today, it’s $636,000.

In NSW, it has climbed from $150,000 to $771,000 while in Victoria, it has increased from $123,000 to $617,000.

Banks, fearing sticker shock among customers, have extended mortgage repayment periods to 30 years from the traditional 25 years.

These mortgages do not include the “bank of mum and dad”, which is only eclipsed in size by the loan books of Commonwealth Bank, Westpac, National Australia Bank and ANZ.

Since 2002, the combined value of owner-occupier mortgages held by the big four has climbed from $167 billion to $1.1 trillion while investor loans have jumped from $45.5 billion to $559 billion.

Hutley says housing affordability has reached a crisis level across a range of metrics that should have young Australians in constant protest.

“This is not only untenable, it represents a massive failure of young Australians by all levels of government over a period of decades, that has resulted in enormous economic, social and even environmental costs and is entrenching intergenerational inequality,” she says.

“Such outrageous neglect of Millennials, in particular, makes me wonder why they are not marching in the streets.”

Eslake accuses the political class of shedding crocodile tears for aspiring first home buyers, who number about 100,000 a year and would benefit most from a fall in house price inflation relative to income.

“Whereas politicians know that at any point in time there are more than 11 million Australians who own their own home, and at least 2 million who own at least one investment property: and that’s 11 to 13 million votes for policies that would keep house prices rising at a faster rate than incomes,” he says.

Housing affordability has become a federal political firestorm unlike at any other point in a generation, while the states, led by NSW Premier Chris Minns and Victoria’s Jacinta Allan, are moving in unprecedented ways on the issue.

The federal government alone has announced more than $32 billion in programs, including grants to fast-track planning and infrastructure, more social housing, and specialist programs for remote Indigenous communities and veterans.

Treasurer Jim Chalmers says the government’s highest priorities are the cost of living and housing.

“Wages growth is also a really important part of addressing cost of living generally, and annual real wages growth is back under this government after a decade of deliberate stagnation and suppression from our predecessors,” he says.

The Coalition has announced plans to channel $5 billion towards infrastructure for new housing estates while re-heating its 2022 election promise to allow first-time buyers to access part of their superannuation.

Shadow treasurer Angus Taylor, who this week used a speech to argue a key challenge for wealth creation was making home ownership “achievable again”, says locking people out of home ownership is both morally wrong and economically reckless.

“A collapse in home ownership has profound implications not just for our aspirational character, but the costs of our retirement system,” he says.

Greens housing spokesman Max Chandler-Mather says prices will continue to outgrow wages under the policy prescriptions of the government and the Coalition.

He says wages need time to catch up.

“The only way we are going to get house prices to stabilise is by ending the massive tax breaks for property investors, and get the government back in the business of building affordable housing at a scale that can affect prices,” he says.

No side of politics is prepared to argue that house prices should fall or even stop climbing. At the National Press Club last month, teal independent Allegra Spender – who represents the seat of Wentworth, which has some of the country’s most expensive housing – said wages needed to rise rather than prices fall.

As Eslake notes, the vested economic self-interest of existing home owners is politically insurmountable.

Of the estimated $16.5 trillion in wealth held by Australian households, two-thirds, or $11.2 trillion, is tied up in housing and land. The next largest pot of wealth is super at $3.9 trillion.

The nation’s biggest banks would face huge problems if home values, supporting $1.7 trillion in mortgages, started to fall.

But the surge in prices relative to wages has enormous economic and social costs.

Hutley says insecure housing leads to poorer education levels, mental and physical health plus labour force flexibility.

The tax system inflates the importance of housing as an asset class, crowding out more productive investment.

“The truly tragic thing is that there are no silver bullets. It may take another generation to solve the problem, assuming politicians decide to act comprehensively,” she says.

The gulf between wages and house prices has occurred on the watch of the Reserve Bank. A step-down in interest rates from the mid-1990s to mid-2000s, due largely to the RBA bringing inflation under control, increased Australians’ borrowing power.

The post-global financial crisis world of ever lower interest rates inflated the borrowing power to which Australians, and banks, have become accustomed.

Eslake says the ultimate cost is being borne by young Australians and those yet to be born. Home-ownership rates among 25- to 34-year-olds are back to where they were in 1947 – and could deteriorate further.

“The situation could be about to get even worse, if that’s possible, when the Reserve Bank starts to cut official interest rates,” he concludes.